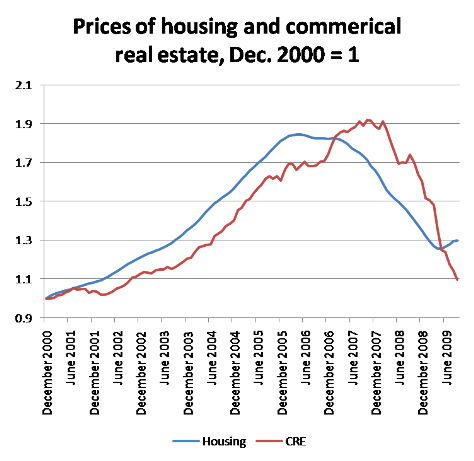

Megan McCardle at The Atlantic Monthly has an interesting column on the commercial real estate crash, and what it might imply about the residential crash. It turns out, the boom and bust of commercial property follows pretty much exactly the same trajectory as the residential market. Echoing Paul Krugman’s piece, McCardle points out that the overlapping trends undermine any number of explanations:

{kind=link}

Yet we can’t blame this on predatory lenders tricking the unsophisticated into unwise loans, because these were basically all professionals. Nor can we argue that banks were willing to write toxic loans because they were just going to sell the garbage off to investors; a much smaller percentage of commercial mortgages were securitized (though that percentage did increase as the bubble inflated). And we certainly cannot blame them because they “should have known better” than their borrwers, who usually had more experience than the banks in pricing commercial real estate.

Somehow, everyone got stupid all at once.

So what was it?

To answer that question, John Cassidy of The New Yorker headed to Chicago to chat up the big thinkers from The Chicago School about what they think. Although the beginning presents what I think is a misleading caricature of Chicago versus the Keynesians in a black hat, white had fashion, it’s interesting to hear what the likes of Richard Posner, Gary Becker, John Cochrane, and Eugene Fama view the crisis. I especially liked reading about Fama, who canceled his subscription to The Economist because he was tired of reading the word “bubble.”

His piece is currently gated, but I have a copy if you care to take a look.