For those of you who enjoyed part I, follow this link to part II. The first four minutes provide part II, and the remaining six minutes involves a discussion with the creators. Enjoy.

L.W. Burdeshaw, an insurance agent in Chipley, told the St. Petersburg Times in 1982 that his list of policyholders included the following: a man who sawed off his left hand at work, a man who shot off his foot while protecting chickens, a man who lost his hand while trying to shoot a hawk, a man who somehow lost two limbs in an accident involving a rifle and a tractor, and a man who bought a policy and then, less than 12 hours later, shot off his foot while aiming at a squirrel.

“There was another man who took out insurance with 28 or 38 companies,” said Murray Armstrong, an insurance official for Liberty National. “He was a farmer and ordinarily drove around the farm in his stick shift pickup. This day – the day of the accident – he drove his wife’s automatic transmission car and he lost his left foot. If he’d been driving his pickup, he’d have had to use that foot for the clutch. He also had a tourniquet in his pocket. We asked why he had it and he said, ‘Snakes. In case of snake bite.’ He’d taken out so much insurance he was paying premiums that cost more than his income. He wasn’t poor, either. Middle class. He collected more than $1-million from all the companies. It was hard to make a jury believe a man would shoot off his foot.”

It’s not often that I come across source material like this that I will use every single time a topic comes up in class. I tested it out on Econ 300 today and I daresay the image is a lasting one.

So you think the little fishies are cooperating? Not so much… It’s actually a straightforward prisoners’ dilemma problem: If all the little fish would scatter at the same moment, most would escape, because there are so many and the predators are few. But if I expect YOU to take off, I should stay in the ball. One or two fish trying to escape will be caught. And if I expect you to stay in the ball…I should STILL stay in the ball.

The LSB program burst on this year’s scene in the form of the Alternative Investments Summit on Sunday. (Here is the announcement.) I saw many new faces, which is great: students discovering the program. I know that students always learn a lot from these events. (Proof by Introspection: I myself always learn a lot from these events. Therefore, so do students. Q.E.D.) I enjoyed hearing from Messrs. Spaeth, Allweiss and Perille, who said that Private Equity people simply have more fun. Anyway, my quick summary:

Your liberal learning has gravity,

Match it with years in an industry,

Get credit training

(It isn’t too draining)

You’re ready to try private equity.

The case studies always add an element to this event that infuses it with that real-life excitement that I wish more of my classes had. As often in the past, Mr. Perille put his money where his mouth was, and offered up a small percentage of the proceeds of his latest deal for the best team in the room. After over an hour of reading and vibrant discussion, each team had to take the stage in turns. The winning team: Aimen, Minh, Ranga, Regina, Vishvesh. They showed us quick and smart analysis, presented cogently. The judges, Sandy and Kirk Ryan ’83 were visibly impressed. Their classmate, Jonathan Bauer ’83 is leading the next Summit, on Management Consulting–coming up on January 15th. That one’s always a riot, featuring–again–some hands-on case study work. No $100 prize in the past, though. That does give you a hint about one difference between consulting and private equity.

A recent EconTalk has John Quiggin, left-of-center author of Zombie Economics, discussing ideas with Russ Roberts, moderator and pro-market guy. Quiggin names his book such because he asserts that there are many economists clinging to ideas that have been thoroughly thrashed and should be discarded, yet they continue to emerge and thrive. Foreign Policy has a summary of Quiggin’s five most egregious “undead” ideas:

I'm an idea zombie

The Great Moderation: the idea that the period beginning in 1985 was one of unparalleled macroeconomic stability that could be expected to endure indefinitely.

The Efficient Markets Hypothesis: the idea that the prices generated by financial markets represent the best possible estimate of the value of any investment. (In the version most relevant to public policy, the efficient markets hypothesis states that it is impossible to outperform market valuations on the basis of any public information.)

Dynamic Stochastic General Equilibrium (DSGE): the idea that macroeconomic analysis should not be concerned with observable realities like booms and slumps, but with the theoretical consequences of optimizing behavior by perfectly rational (or almost perfectly rational) consumers, firms, and workers.

The Trickle-Down Hypothesis: the idea that policies that benefit the wealthy will ultimately help everybody.

Privatization: the idea that nearly any function now undertaken by government could be done better by private firms.

Roberts certainly doesn’t agree with Quiggin’s overall assessment, though they do find much to agree on. This is a great EconTalk for those who think that economists all drink from the same cup.

Econ 300 students might listen to the part about the Efficient Markets Hypothesis and compare it to what Landsburg says in Chapter 9.

And, if you like the dead-undead econ riff, you might check out Todd Buchholz’s now-classic, New Ideas from Dead Economists.

Rational ignorance is a common theme of economists thinking about voting and the electorate, but what about willing ignorance? That’s the gist of this Schumpeter quotation:

“[T]he typical citizen drops down to a lower level of mental performance as soon as he enters the political field. He argues and analyzes in a way which he would readily recognize as infantile within the sphere of his real interests…”

Here is some more background on that quote. It is certainly consistent with the overarching theme of Capitalism, Socialism and Democracy that capitalism might die out due to lack of enthusiasm from its principal beneficiaries.

The accompanying illustration is from the legendary political cartoonist, Herblock. I snagged both the quote and the picture from the Spirit of Moderation blog.

The Federal Reserve Bank of St. Louis (which you know offers numerous publications that contain a fabulous array of macroeconomic data) recently announced a contest to produce a YouTube video that helps explain the factors of production in general and the role of entrepreneurs in particular to high school students. For some of you, this is too good an opportunity to pass up. Go to St. Louis Fed to learn the details.

After yesterday’s spirited discussion of the nature of the long-run supply curve, tomorrow we will kick off with the classic brownie problem:

Brownies sell for $12 a dozen and are available only in packs of a dozen. You choose to buy two packs a month. If sellers begin offering brownies at $1 each, what can you say about the quantity you will buy?

The Lawrence Scholars in Law kicked off in style with a capacity crowd (35-40 students) and a festival-type atmosphere, with about 15 students joining us for dinner. As I said in my introductory remarks, the alumni talent on hand for our panel was extraordinary. Each is a lawyer and a member of the Lawrence board of trustees, and each is very enthusiastic about he prospects for the LSL program.

A couple of points emerged from the discussion. The first is that there is no right major that you need to choose to apply. Our four panelists came from four different majors — history, government, economics, and piano performance. The second theme seemed to be that a law degree opens up many doors, not just the door to the big law firm.

Panelist Jeff Riester also pointed prospective law students to Law School: Getting In, Getting Out, Getting On, by Michael Ariens. This seems like a good resource, and pre-law advisor Steve Wulf and myself will hold onto it if you care to take a look at it.

We are planning one LSL per term this year, and we would like to encourage you to provide us with feedback, as well as input into content for future programs.

Highway 26The frozen chickens add a surrealist touch

The weather was not ideal for driving across Wisconsin, but the unusual conditions produced some amazing scenery.Before the Forum began, I had a chance to catch up with a friend, Daniel Barolsky, who was a Postdoctoral Fellow at Lawrence during the first year of the Fellows program. We all know that the first crop of Fellows was the best. I came in the second year of the program as a Fellow, so Daniel and I overlapped two years at LU. Anyway, we sat down in the Bushel and Peck’s, which is the center of activity in Beloit. It is a very interesting place–they have gourmet groceries, coffee, food, and ambience conducive to conversation. If you go, do stick to American coffee–that’s definitely their forte. If you get their bottomless cup, you will end up going through the art gallery in the back, which leads to the restroom. Oh, and the frozen chickens are stored back there, too.

The Forum itself started with a panel on Entrepreneurship and the Liberal Arts. Our own Prof. Finkler presented as part of a distinguished panel, describing the great many things we do in the name of I&E at Lawrence. He started with an image of the “Creative Instruction” cup that I presented to Prof. Gerard to signify his Chief of Schumptoberfest title. Prof. Finkler then summarized Schumptoberfest, In Pursuit of Innovation, Entrepreneurship and Finance, Entrepreneurship in the Arts and Society, and the many ways we build innovation and entrepreneurship into our courses at LU (including the upcoming Economics of Innovation course–watch this space for updates!) He also talked about the center we are developing, the Lawrence Innovation Bridge, where student ventures will have a space to grow. Robyne Hart from the ACM’s Chicago BES program also presented, outlining the indisputable advantages of being in Chicago, a hub of innovation and entrepreneurship. Consider making that a part of your Lawrence experience. From Wake Forest University, Betsy Gatewood presented on education, entrepreneurship and the liberal arts. She should know, being the Director of their Office of Entrepreneurship and Liberal Arts. They have an astounding variety of courses in all disciplines that relate to Entrepreneurship–take a look and let everyone at Lawrence know that you’d like to see more of that stuff here, too. Finally, Beloit’s own Jerry Gustafson gave an eloquent, entertaining, erudite, evocative and overall excellent monologue on entrepreneurship and education. We’ll see if we can make that available to you somehow. Finally Israel Kirzner himself reacted to what had been said. He thanked the panelists for all he had learned from their talks, pointing out that much of it was “refreshingly new” to him. Then he went on to make a distinction between studying the role of entrepreneurs in the economy (what he has done) and studying entrepreneurship, what makes an entrepreneur, etc.

The panel on Kirzner, incl. Kirzner

Prof. Kirzner reiterated that distinction in the evening panel discussion on his work. The participants were (from left to right in the pic) Roger Koppl, Deirdre McCloskey, Virgil Storr, and Israel Kirzner. Much was said about expertise, entrepreneurship, piracy and shipwrecking, but to me the most interesting comments came from McCloskey, who started by describing, in the way of a confessional, here transformation from Chicago-school Samuelsonian anti-entrepreneurship economist to a fan of Kirzner. Max U, the protagonist of price theory, is a sociopath, says McCloskey, and we need a much better model of Human Action than that. Of course she has done much to round out our view of human action in her several books, the most recent of which is Bourgeois Dignity: Why Economics Can’t Explain the Modern World . She went on to reiterate the argument that some of us know from Schumptoberfest: Samuelsonian equilibrium economics has no place for the entrepreneur, because equilibrium looks at what happens after the entrepreneur’s work is done. As Jerry Gustafson put it, “by the time the theorist arrives on the scene, the entrepreneur has vanished.” There was much talk about what exactly Kirzner meant by “alertness.” He himself put it as “knowing what is around the corner,” and reminded us that by definition it cannot be taught. Apparently that comment (it is not possible to teach entrepreneurship) was made to him by Baumol many years ago. In response, Jerry Gustafson and others made the argument that neither is it possible to teach someone how to be a virtuoso violinist or pianist–but it certainly is possible to enhance one’s innate abilities in those areas. So it is with entrepreneurship: the true entrepreneur is born, not made, but we can certainly enhance those aptitudes through education. Perhaps more importantly, having entrepreneurship programs opens students’ minds (alerts them to) to the possibility of pursuing an entrepreneurial life. Gustafson added that having an entrepreneurship center like CELEB gives students an opportunity to try their hand at entrepreneurship in a safe place, where failure is not catastrophic and there is friendly help that makes starting a venture a learning experience. Our own dreams of the Lawrence Innovation Bridge go along these lines, too.

If you have any questions or comments about any of this stuff, click below and comment, or talk to us.

Slate hasa very nice piece on investors buying US Treasury bonds that yield negative interest rates! Now, why on earth would someone buy a bond with a negative interest rate? Though the answer is not complicated, it is more than a sentence explanation, so I will let you read it for yourself. Let me just say, inflation is involved.

For those of you not versed in corporate finance (or “core-fin,” as it’s known), the article provides a good summary of how debt markets work.

The LSB season opens this year with the Alternative Investments and hedge funds event, this coming Sunday. Bob Perille himself is leading this one, and it’s promising to live up to the high standards we have come to expect from him and his colleagues. This year’s event will be different from last year’s, however, so come even if you attended last year. Jason Spaeth is skype-ing in, participating as an LSB panelist for the first time, and he is going to be introducing the industry. Another good reason to come is the actual, real-life, taken-from-the-trenches (or tranches?) offering memoranda that Mr. Perille always brings. You get to work on those in teams, and, in the past, Mr. Perille has offered a prize of $100 for the team with the best presentation on their “mini case study.” So don’t miss your chance to learn something interesting about the world you live in–whether you want to become a private equity whiz or not.

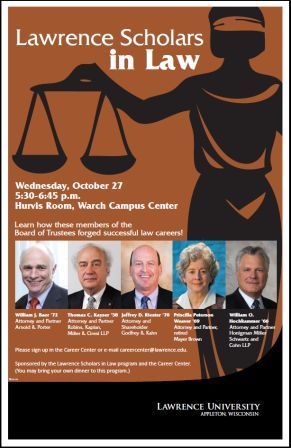

Firmly on the coattails of the extraordinary success of the Lawrence Scholars in Business program, the inaugural Lawrence Scholars in Law event kicks off at 5:30 on Wednesday, October 27 in the Hurvis Room of the Warch Campus Center.

Who should attend this session? I would suggest anyone who is thinking about a law career should clear their schedule for this one. Also, anyone who isn’t sure about their own career ambitions might consider poking her head in. Many students these days work for a few years before returning to pursue a law degree. And liberal arts majors generally, and economics majors in particular, have potential to succeed.

The talent on hand for this program is exceptional. We have five successful attorneys, each a partner or a shareholder (what’s the difference? Good question to ask) with a major law firm. And each with a member of the Lawrence University Board of Trustees. They are:

William J. Baer ’72 Attorney and Partner: Arnold & Porter

Thomas C. Kayser ’58 Attorney and Partner: Robins, Kaplan, Miller & Ciresi LLP

Jeffrey D. Riester ’70 Attorney and Shareholder: Godfrey & Kahn

Priscilla Peterson Weaver ’69 Attorney and Partner, retired: Mayer Brown

William O. Hochkammer ’66 Attorney and Partner: Honigman Miller Schwartz and Cohn LLP

Professor Gerard will also be on hand to moderate.

Please sign up in the Career Center or e-mail careercenter@lawrence.edu to make your intentions known.

You are welcome to bring your dinner to the program. Or, better yet, plan to dine with the five panelists afterwords.

The Schumptoberfest celebration was a smashing success, with at least one of us understanding the Williamson debt-equity financing argument a little better at the end than at the beginning. Thanks to all those who participated, especially Professor Galambos, who took time out from his sabbatical leave to read “100” pages and keep me in line.

As per usual with these events, we received word that there were some items left behind. Here is a partial accounting: a set of dentures, a hearing aid, “a leather whip, a live rabbit, a tuba, a ship in a bottle, 1,450 items of clothing, 770 identity cards, 420 wallets, 366 keys, 330 bags and 320 pairs of glasses, 90 cameras and 90 items of jewellery and watches.”

Last year’s Entrepreneurship in the Arts & Society course included An Evening of Baroque Dance and spawned the formation of Lawrence Baroque on campus. Lawrence Baroque is one of many that is inviting you to stop by the Lawrence Chapel Tuesday at 8:30 p.m. to try out some of the new acquisitions from the James Smith Randolph collection of early winds! The invitation is extended to all, from professionals to novices. So stop by if you can spare a major second.

The event is part of the Lawrence University Collective of Early Music (LUCEM) the campus early music initiative at Lawrence, and, in addition to Lawrence Baroque, the Lawrence University Musicology Association, Harmonia, and Alta Capella are also involved.

That’s the title of Monday’s panel in the Hurvis Room of the Warch Campus Center at 6:30, and it should be a corker. Ever since the Supreme Court decided Citizens United v. Federal Election Commission this past January, all you-know-what has broken loose about money in U.S. politics. The president famously called out the court in his State of the Union address, with Justice Alito brazenly mouthing the words, “not true.” And it hasn’t gotten any friendlier from there. Now, that’s entertainment!

The event will cover a lot of ground, including these Common Cause talking points:

Redistricting Reform

Disclosure of interest-group ads and other outside spending

Public Financing of Wisconsin Supreme Court and other state elections

Campaign Finance Reform in Wisconsin after the U.S. Supreme Court decision on Citizens United vs F.E.C.

We will welcome panalists from both sides of the aisle, including State Representatives Penny Bernard Schaber (D-Appleton) and Dean Kaufert (R-Neenah), Andrea Kaminski from the League of Women Voters, and Jay Heck of Common Cause in Wisconsin.

Given the number of co-sponsors, I’m guessing there is ample interest. The co-sponsors are: the Lawrence Government Department, the College Republicans, the League of Women Voters of Appleton, League of Women Voters of Wisconsin, the Education Fund, the American Association of University Women – Appleton Branch, and the Wisconsin Alliance for Retired Americans.

I am moderating the event, so I hope to see you there.

Describe the industrial structure and to evaluate the interrelationships between firm size, market structure, and innovation in your assigned industry. You should address the following questions:

What are the strengths and weaknesses of using a model of “perfect competition” (many firms, homogenous products, low switching costs, price competition) to characterize the industry?

What is the “structure” of your industry? Is it dominated by a few firms (concentrated)? Or are there many firms?

How would you characterize innovation in your industry? Is it particularly dynamic or innovative? Are we observing new products or new processes? Are the firms that come up with the ideas the same as those implementing these ideas?

Would you say your industry characterized by managerial or entrepreneurial capitalism? That is, how is innovation funded in this industry?

Next, determine where you come down on the “Schumpeter hypothesis” in terms of market structure and innovation. Write down a thesis statement and three supporting points to argue for or against Schumpeterian-type arguments. These might include:

R&D projects have high fixed costs that can only be covered by industry with robust revenue streams.

Economies of scale and scope foment innovation.

Diversified firms are in superior position to identify and exploit unforeseen innovation opportunities.

Large firms are able to spread the R&D risks across many projects.

Large firms have more favorable treatment in obtaining external financing.

Firms with market power make higher profits, and can use retained earnings to finance R&D from own profits.

Firms with market power have fewer rivals and thus are more able to appropriate returns from innovation, bolstering the incentive to innovate.

We will spend Sunday morning talking about these industries. We will begin by going around and providing a brief description of each industry. After that, each group will state its thesis and then discuss its supporting arguments.

William James Adams, (2006) “Markets: Beer in Germany and the United States,” Journal of Economic Perspectives, 20(1): 189-205

Emek Basker (2007) “The Causes and Consequences of Wal-Mart’s Growth.” Journal of Economic Perspectives, 21(3): 177–198

Kal Raustiala and Christopher Jon Sprigman (2009) “The Piracy Paradox Revisited,” Stanford Law Review, 61(5).

Following up on Chapter VII of Capitalism, Socialism, & Democracy from last time, we move on to some rather more modern treatments of the economics of innovation. We start with Professor Galambos’ and a slightly modified version of the primer he gives to his students in his excellent course, In Pursuit of Innovation(coming this winter).

Galambos wades through some basics of innovation policy and the industrial enlightenment before arriving at the question of allocative efficiency on pages 4 and 5. Again, the conventional treatment is that there is a tradeoff between the promise of monopoly profits and the efficiency properties of competitive industries. And, recall, this is a tradeoff that Schumpeter explicitly rejects.

Come one come all to Wednesday’s talk by Professor Finkler about parallels between the Great Depression of the 1930s and the Great Recession that was recently declared over. The presentation will highlight the lessons to be learned from the Great Depression and to what degree we have learned them. The talk will take place in Steitz Hall 102 at 4:30, Wednesday, October 20th.

So you think the little fishies are cooperating? Not so much… It’s actually a straightforward prisoners’ dilemma problem: If all the little fish would scatter at the same moment, most would escape, because there are so many and the predators are few. But if I expect YOU to take off, I should stay in the ball. One or two fish trying to escape will be caught. And if I expect you to stay in the ball…I should STILL stay in the ball.

So you think the little fishies are cooperating? Not so much… It’s actually a straightforward prisoners’ dilemma problem: If all the little fish would scatter at the same moment, most would escape, because there are so many and the predators are few. But if I expect YOU to take off, I should stay in the ball. One or two fish trying to escape will be caught. And if I expect you to stay in the ball…I should STILL stay in the ball.

Last year’s Entrepreneurship in the Arts & Society course included An Evening of Baroque Dance and spawned the formation of Lawrence Baroque on campus. Lawrence Baroque is one of many that is inviting you to stop by the Lawrence Chapel Tuesday at 8:30 p.m. to try out some of the new acquisitions from the James Smith Randolph collection of early winds! The invitation is extended to all, from professionals to novices. So stop by if you can spare a major second.

Last year’s Entrepreneurship in the Arts & Society course included An Evening of Baroque Dance and spawned the formation of Lawrence Baroque on campus. Lawrence Baroque is one of many that is inviting you to stop by the Lawrence Chapel Tuesday at 8:30 p.m. to try out some of the new acquisitions from the James Smith Randolph collection of early winds! The invitation is extended to all, from professionals to novices. So stop by if you can spare a major second.

Following up on Chapter VII of Capitalism, Socialism, & Democracy from last time, we move on to some rather more modern treatments of the economics of innovation. We start with Professor Galambos’ and a slightly modified version of the primer he gives to his students in his excellent course, In Pursuit of Innovation (coming this winter).

Following up on Chapter VII of Capitalism, Socialism, & Democracy from last time, we move on to some rather more modern treatments of the economics of innovation. We start with Professor Galambos’ and a slightly modified version of the primer he gives to his students in his excellent course, In Pursuit of Innovation (coming this winter).