In this, the 500th post on the Lawrence Economics Blog, we bring you a story from the NYT on the statistical value of life. Indeed, as anyone in an environmental economics or policy course knows, the “value” placed on saving a statistical life (VSL) is associated with reductions in risk levels that decrease the probability of being killed (i.e., from reducing the number of purple balls in your urn).

In this, the 500th post on the Lawrence Economics Blog, we bring you a story from the NYT on the statistical value of life. Indeed, as anyone in an environmental economics or policy course knows, the “value” placed on saving a statistical life (VSL) is associated with reductions in risk levels that decrease the probability of being killed (i.e., from reducing the number of purple balls in your urn).

This VSL is pivotal in determining the benefits of many non-economic regulations, and many federal agencies have increased the value used in benefit assessment in the past few years.

The Environmental Protection Agency set the value of a life at $9.1 million last year in proposing tighter restrictions on air pollution. The agency used numbers as low as $6.8 million during the George W. Bush administration.

The Food and Drug Administration declared that life was worth $7.9 million last year, up from $5 million in 2008, in proposing warning labels on cigarette packages featuring images of cancer victims.

The Transportation Department has used values of around $6 million to justify recent decisions to impose regulations that the Bush administration had rejected as too expensive, like requiring stronger roofs on cars.

That is the salient point of the article; the rest mostly gets down to talking about the prospects and problems of using VSLs in the first place. If you are reading this, you probably know already.

The fashion industry, a $200 billion industry in the United States alone, is comprised of nearly 150,000 establishments, ranging in size from large fashion houses to smaller start-ups. Although there are a large number of firms competing in the industry, according to the 2002 Census, five percent of firms in the clothing industry accounted for twenty percent of total revenue and sales. These large firms, , also play an important role in the diffusion of new design trends and the continuation of induced obsolescence, the dynamic force driving the fashion cycle forward; the influence of large firms contributes to the top-down structure of the industry.

The fashion industry, a $200 billion industry in the United States alone, is comprised of nearly 150,000 establishments, ranging in size from large fashion houses to smaller start-ups. Although there are a large number of firms competing in the industry, according to the 2002 Census, five percent of firms in the clothing industry accounted for twenty percent of total revenue and sales. These large firms, , also play an important role in the diffusion of new design trends and the continuation of induced obsolescence, the dynamic force driving the fashion cycle forward; the influence of large firms contributes to the top-down structure of the industry.

n the second post here, I will simply concentrate on Chapter VII of Capitalism, Socialism, and Democracy, and try to tie together some themes for the weekend. For our purposes, I have numbered the paragraphs 1-13.

n the second post here, I will simply concentrate on Chapter VII of Capitalism, Socialism, and Democracy, and try to tie together some themes for the weekend. For our purposes, I have numbered the paragraphs 1-13. This is a first in a series of short posts to guide the Schumptoberfest readings. I included these readings literally to give you an introduction to Schumpeter and the “Schumpeterian Hypotheses.”

This is a first in a series of short posts to guide the Schumptoberfest readings. I included these readings literally to give you an introduction to Schumpeter and the “Schumpeterian Hypotheses.”

We would like to engage students who have a good understanding of micro theory and are interested in innovation and entrepreneurship. The readings dovetail nicely with my Economics 400 (IO) and 450 (theory of the firm) courses.

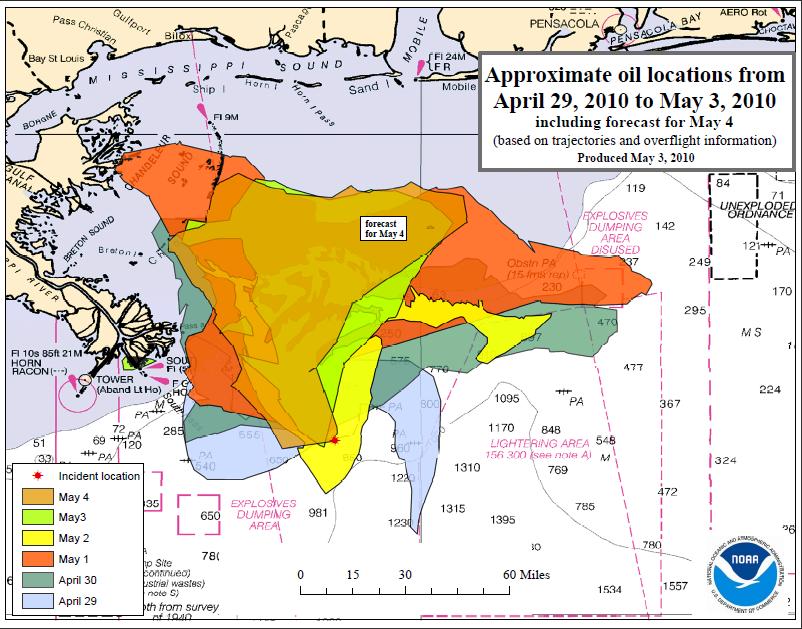

We would like to engage students who have a good understanding of micro theory and are interested in innovation and entrepreneurship. The readings dovetail nicely with my Economics 400 (IO) and 450 (theory of the firm) courses. BP’s stock, which traded at a 52-week high of $62.38 on Jan. 19, 2010, closed on June 1 at $36.52 a share, down 15% on the day. The post-spill sell-off has wiped out some $68 billion of BP’s market value, knocking it down to $114 billion. With the stock now in the cellar, some speculation even has it that BP may attract a buyer.

BP’s stock, which traded at a 52-week high of $62.38 on Jan. 19, 2010, closed on June 1 at $36.52 a share, down 15% on the day. The post-spill sell-off has wiped out some $68 billion of BP’s market value, knocking it down to $114 billion. With the stock now in the cellar, some speculation even has it that BP may attract a buyer. He finds big impacts. The red line in the picture is his estimate of the time series of BP’s stock price without the spill, and the black line is the actual price. Seems like a big effect.

He finds big impacts. The red line in the picture is his estimate of the time series of BP’s stock price without the spill, and the black line is the actual price. Seems like a big effect. The

The